Even before the coronavirus sent the global economy into a tailspin, private equity funds were training their focus inward on creating value for their portfolio companies and signaling more interest in distressed investing. The onset of the pandemic has only magnified this trend. Since March, when COVID-19 became a palpable threat to lives and businesses in the United States, most private equity funds have been scrambling to keep their portfolio companies afloat.

Meanwhile, volatility in the markets has given the industry the correction in valuation they have been looking for. Although we expect many to remain in triage mode for the short term, distressed funds and those with dry powder are actively looking for both quality and value investment opportunities—of which there will be many. What makes the current environment so unique is that—with the exceptions of businesses and industries that touch “essential†services—no company or industry has escaped the effects of COVID-19. The denominator for so many companies in distress today is not faulty strategy or feeble management teams; it is the sudden lack of liquidity deriving from a precipitous drop in demand.

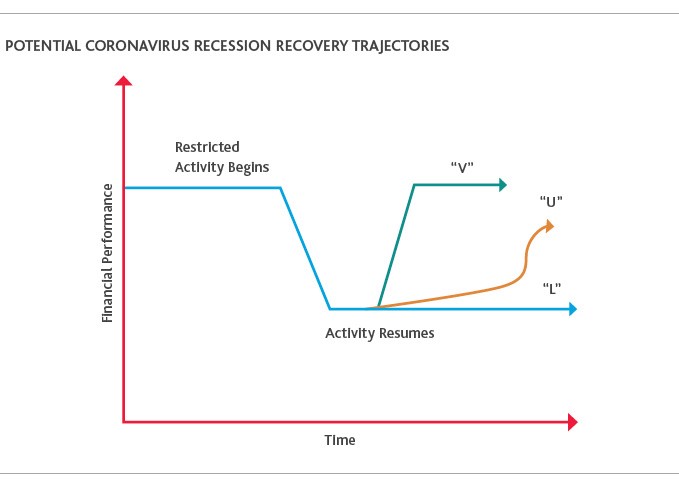

While it may be easier to find discounted deals, it will be harder to value them. Though prior recessions offer some concept of what an eventual recovery might look like on paper, the nature of this particular economic rebound, when it happens, is unknown. There is no clarity around when the health threat might subside and allow for a resumption of “normal†activity and, thus, no clarity around when the economy might recover.

Detailed and rigorous due diligence has always been key to a successful acquisition, but now is a critical component in valuing a target with some confidence.

Valuing a Target During a Pandemic

Before the crisis hit, private equity fund managers already were trending toward becoming industry specialists. To properly value a target, fund managers will need a deep understanding of a company’s operational universe—everything from internal controls and processes to customers, the supply chain, access to raw materials, and the unique dynamics of the industry in which that company operates.

For companies in industries that have significant exposure to the turbulence caused by the pandemic—for example, supply chain disruption to the manufacturing and distribution or retail industries—operational diligence should include:

- An investigation into a target’s contracts with third-party suppliers to help determine the target’s force majeure and insurance clauses

- An evaluation of the extent to which the target’s various buyers have been affected and what the recovery timeline may be for those markets

- A determination of what employee and contractor safety measures are in place to keep the business running should another pandemic wave hit

- A review of any employment or labor issues resulting from the pandemic that could prove problematic or lead to litigation

A fund’s quantification of the impact of the coronavirus on earnings before interest, taxes, depreciation, and amortization (EBITDA) should first determine whether the damage to the target’s operations is reparable. If it is, then funds should develop an operating plan that outlines a clear path to generating returns.

The scope of traditional valuation techniques, such as discounted cash flow and benchmarking against publicly traded companies’ valuations, is less equipped to account for the uncertainty and volatility in the markets today.

Any financial projections should include a range of uncertainty outcomes, models of what the domino effect may be from the impact of a pandemic on different aspects of a target’s business, and the ways in which that domino effect will cascade to the target.

In order to get a financial picture of a target, it has become customary to normalize historical earnings, which has involved pro forma EBITDA adjustments that reflect the current run rate of the business.

Tax & Other Considerations

Any fund seeking a distressed transaction should engage tax advisors at the beginning of the process. Not only does this ensure proper tax structure of the deal but it enables funds to identify a target’s beneficial tax attributes, such as tax basis and net operating losses (NOLs) and carryforwards. Parameters around the usage of the latter two changed with the passage of the Coronavirus Aid, Relief and Economic Security (CARES) Act, and transactions with distressed entities should be sure to quantify those changes.

With the exception of a handful of businesses that have benefited from the pandemic, most have been significantly negatively affected. The restaurant, hospitality and airline sectors have been especially hard hit. While there are federal relief measures available, the private equity industry has largely been excluded from them, though there are some options for portfolio companies.

Funds should also consider which sectors may emerge as “winners.†The healthcare and technology sectors are typically referred to as “recession resilient,†but given the potential paradigm shift that may result from the pandemic—remote working, businesses pivoting to accommodating audiences and consumers with whom they cannot have contact—there is real potential for digital commerce, telemedicine and automation to be positioned for success.

Adapting New Procedures for the New Normal

Both the challenges and the urgency to assess targets with some accuracy are greater today. Distressed diligence can be a fast-paced process. Private equity funds and targets that have already begun to fold digitalization or, better yet, digital transformation into their business operations are better positioned to transact during this time of uncertainty.

The pandemic is triggering unprecedented change. For the due diligence process, this means first and foremost having the digital capabilities to conduct a detailed diligence process and making sure the target company does as well. It also means reevaluating which factors are taken into consideration in financial projections and revenue models, looking at all the possible contingencies in a worst-case scenario.

One thing COVID-19 has taught us is that no business is immune to a pandemic, and the impact on people, businesses and the global economy can be swift and unforgiving. The recovery from the coronavirus crisis remains unclear. Whether the economy will take a V, U, W or L shape, new processes and procedures for conducting due diligence remotely will need to remain in place or be locked and loaded in the event of an analogous global event.

To discuss assessment and optimization of your due diligence practices, tax and other procedural considerations, please contact REDW Valuation Practice Leader, Brian Foltyn.

_____________________________________________________________________________________

Reprinted with permission of BDO USA, LLP. REDW LLC is an independent member of the BDO Alliance USA.